Money Matters with Richard Andrews

In uncertain financial times, the questions that land in Richard Andrews’ inbox are a telling reflection of modern life. They go far beyond pounds and pence, touching on family dynamics, relationships, aspirations, and the everyday pressures of simply trying to stay afloat. From rising fuel costs to the hidden price of holidays, from supporting children to protecting inheritances, and even turning hobbies into income, this week’s column offers grounded, practical advice with a human touch.

Dear Richard, my dad is going mad about the price of petrol. Without making it political, is there any end in sight? What can we do? Aston Basildon

This is a very good question and one many households are asking right now. The reality is that global supply issues have played a major role in pushing up fuel prices. With key shipping routes now reopening, there is some cautious optimism, but it won’t be an overnight fix. Oil and gas supplies take time to stabilise, so realistically we may not see prices return to previous levels until late June or early July. In the meantime, it’s about managing what you can control. Ration your driving where possible, combine journeys, and consider alternatives. A bike, for example, is not only a cost-saving option but also a great way to improve your fitness—just make sure the upfront cost doesn’t outweigh what you’d spend on petrol over the next few months.

Dear Richard, we’re all trying to get away, but what sounds like a cheap holiday often isn’t. Getting to the airport from London can cost as much as the trip itself. Are there any cost-cutting tricks?

Steven Canada Water

Travel to and from the airport can indeed cost a small fortune, and it’s often overlooked when budgeting for a holiday. One of the simplest ways to reduce this cost is by thinking carefully about your flight times. If you can choose flights that align with public transport schedules, you may be able to avoid expensive taxi fares altogether. It’s also worth considering whether you really need to take an express train service or if you have time for a slightly longer journey at a lower cost. Booking in advance is key, as last-minute fares for trains and coaches are typically much higher. Another option to explore is airport parking. It may sound counterintuitive, but for longer trips it can sometimes work out only slightly more expensive than return taxi fares, while offering greater convenience. And of course, there’s always the option of asking a friend for a lift—just remember to return the favour. Do be mindful, however, of drop-off charges at airports, which can add an unnecessary extra cost.

Dear Richard, my teenage son has dropped out of university and says he’s going back next September. He’s on a gap year but currently doing very little and claiming benefits. Is it wrong of me to insist he pays rent, or should I tell him to leave?

Pauline Southend

This is a difficult situation and one that requires a careful balance. My biggest concern is that if your son doesn’t use this time constructively, he may struggle to return to university at all. A year without structure can easily lead to a loss of motivation, and that could have long-term consequences for his education and future prospects. Rather than issuing ultimatums, I would encourage you to focus on guiding him towards making better use of his time. Whether that means finding a job, doing some study to stay in the academic mindset, or developing new skills, the goal is to keep him engaged. Asking him to contribute financially to the household is not unreasonable and can help instil a sense of responsibility. However, telling him to leave could create more problems than it solves and may be something you later regret. Encouragement and support, combined with clear expectations, are likely to be far more effective.

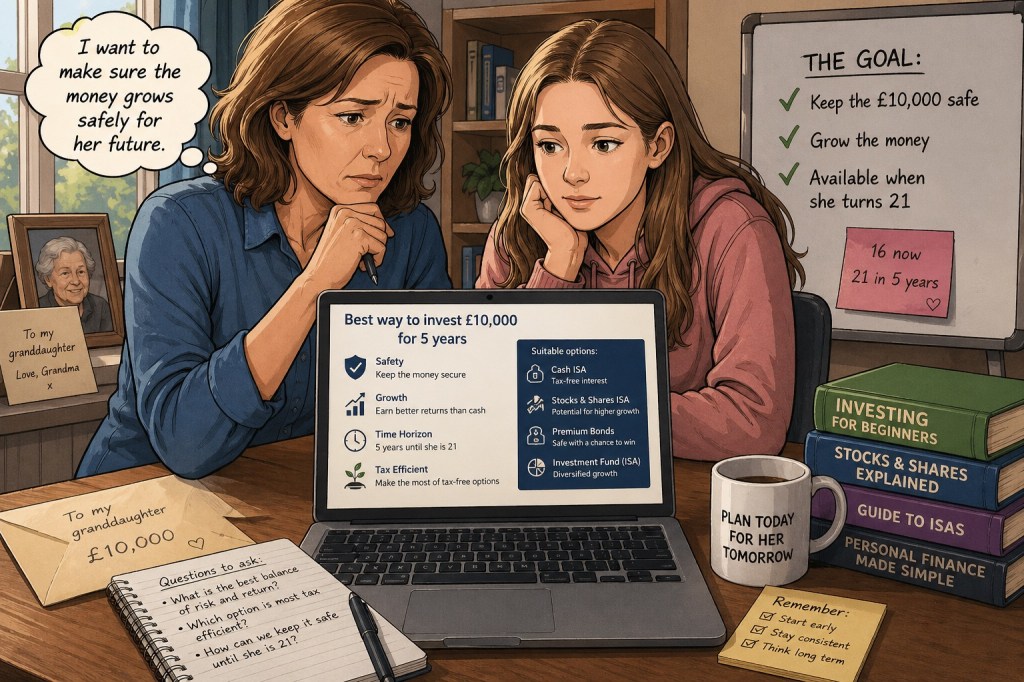

Dear Richard, my daughter has been left £10,000 by her grandmother, with the condition that it is saved until she is 21. She’s currently 16. What is the best way to invest this money?

Margaret Islington

Locking this inheritance away for five years is a sensible and disciplined approach. Fixed-term savings bonds are an excellent option in this scenario, as they offer competitive interest rates while ensuring the funds cannot be accessed prematurely. This not only allows the money to grow but also removes the temptation to spend it too soon. There are a number of providers on the market offering five-year bonds with varying interest rates, so it’s important to shop around and compare options carefully. Always check the terms and conditions to ensure they align with your needs. If your daughter remains in full-time education and has little or no income during this period, the interest earned may also be tax-free, which is an added benefit. By the time she turns 21, she could have a substantial sum to support her future plans.

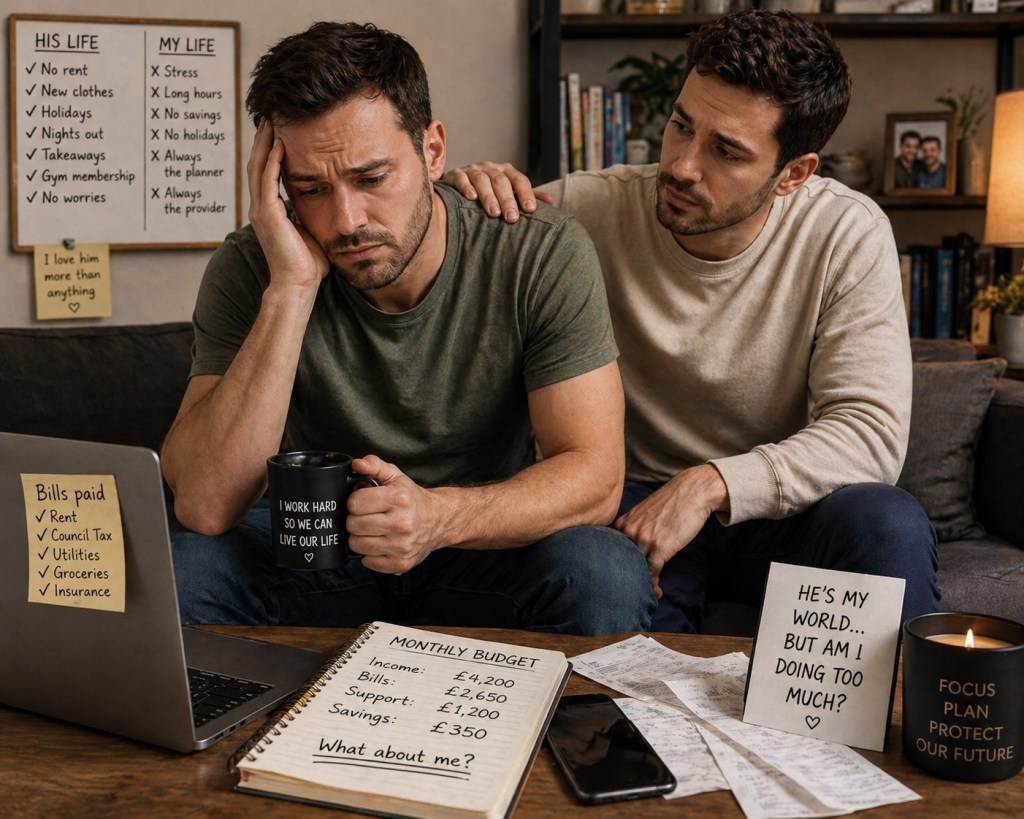

Dear Richard, I supported my partner financially while he was at university, and now he’s working, he still contributes very little. He wants to get married, but I’m concerned about finances. Should I ask for a prenuptial agreement?

Mark London

Supporting your partner through university was a generous and admirable thing to do. However, now that circumstances have changed, it’s only fair that financial contributions are reassessed. Before considering marriage, it’s important to have an open and honest conversation about how household costs are shared. The rising cost of living provides a natural opportunity to revisit this discussion and ensure things are more balanced. Marriage should not be used as a way to gloss over existing concerns, as it can add further complexity to the situation. A prenuptial agreement can be a sensible option if there is a significant difference in assets, but it does require careful handling. Both parties should seek independent legal advice, and the agreement should be made well in advance of the wedding to avoid any suggestion of pressure or coercion. That said, addressing the imbalance in day-to-day finances may resolve your concerns without needing to go down the legal route.

Dear Richard, I’d like to open a small market stall once a week now my eldest is at university. I make jewellery and crafts, and my friends think they’re great. I’ve no idea where to start but want to do it properly. Any advice?

This is a wonderful idea and a great example of turning a passion into a potential income stream. My advice would be to start small and build gradually. Begin by selling to friends or hosting a small jewellery and crafts gathering at home. You might also take commissions, creating bespoke pieces to order. This approach keeps your initial costs low, as you won’t need to invest heavily in stock upfront. If you find there is strong demand and you’re generating a steady income, you can then look at taking a pitch at a local market. Be aware that this will involve additional costs, and availability may vary depending on your area. It’s worth checking your local council’s website for information on market pitches and how to apply. You’ll also need to consider practicalities such as public liability insurance and, depending on your setup, product liability cover. Organisations like the National Market Traders Federation can provide helpful guidance. With careful planning and a measured approach, your hobby could grow into something both rewarding and profitable.

As ever, the common thread running through these questions is that money is rarely just about finances. It’s about choices, relationships, and the future we’re trying to shape. Whether you’re navigating rising costs, supporting loved ones, or taking your first steps into business, a thoughtful and balanced approach will always serve you well.